Content:

The Europe cold sore treatment market is witnessing steady growth due to increased awareness of herpes simplex virus (HSV-1), greater access to over-the-counter antiviral treatments, and a rising number of individuals seeking effective and quick-relief remedies. Cold sores, also known as fever blisters, are caused by HSV-1 and manifest as small, painful blisters primarily around the lips and mouth. Although the virus remains dormant in the body, factors such as stress, illness, sun exposure, or a weakened immune system can trigger outbreaks. The increasing incidence of HSV infections in Europe, coupled with lifestyle changes and greater focus on personal care, are driving market expansion.

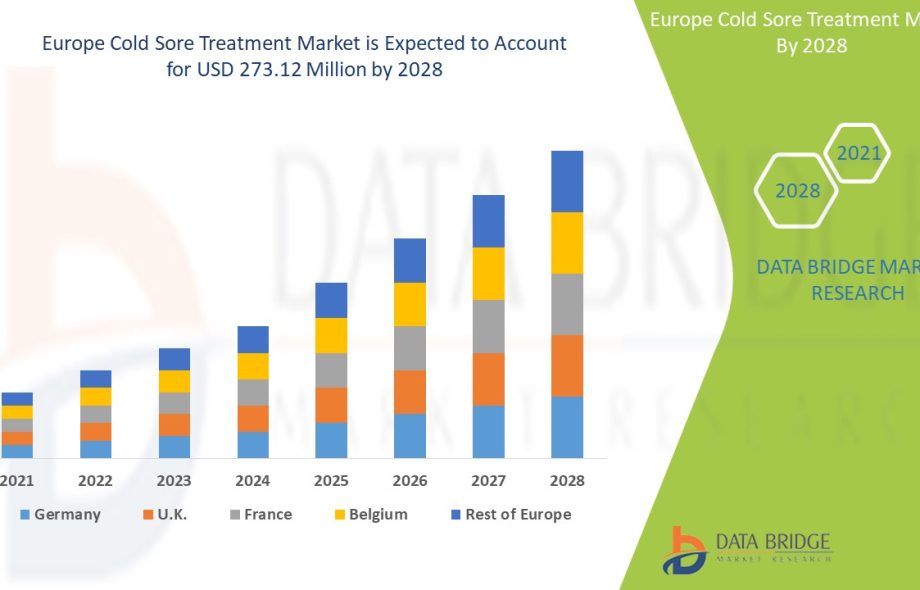

In 2024, the Europe cold sore treatment market was valued at approximately USD 800 million. It is projected to reach around USD 1.3 billion by 2033, growing at a compound annual growth rate (CAGR) of 5.5%. The market’s growth is underpinned by increasing demand for topical creams, oral antiviral medications, and the emergence of innovative delivery methods that offer faster relief and longer protection from recurring outbreaks.

The cold sore treatment market in Europe is segmented by product type, drug class, route of administration, and distribution channel. By product type, the market includes creams and ointments, antiviral tablets, and patches. Creams and ointments continue to hold a significant share due to their immediate soothing effect and widespread consumer preference for topical applications. Antiviral tablets such as acyclovir, valacyclovir, and famciclovir are prescribed for severe or frequent outbreaks and are gaining traction due to their systemic action and ability to reduce healing time. Patches are an emerging category, offering discreet treatment and preventing contamination.

By drug class, the market is divided into nucleoside analogs, antiviral agents, corticosteroids, and others. Nucleoside analogs dominate the market as the most effective class for inhibiting viral DNA replication. Antiviral agents such as docosanol are popular in topical formulations and are frequently used in combination with skin protectants and analgesics. Corticosteroids are prescribed in specific cases where inflammation and pain are severe, although their usage remains limited due to potential side effects.

Based on the route of administration, the market is segmented into topical, oral, and others. Topical administration is the most preferred route among patients with mild symptoms, allowing direct action at the infection site. Oral treatments are mainly used for patients experiencing frequent recurrences or complications. Other routes, including injectable antivirals, are reserved for hospital settings and rare severe cases.

By distribution channel, the market includes hospital pharmacies, retail pharmacies, online pharmacies, and drug stores. Retail pharmacies continue to dominate due to the high demand for over-the-counter products, convenience, and patient preference for self-medication. Online pharmacies are witnessing rapid growth owing to increased internet penetration, digital healthcare platforms, and the availability of products without prescriptions in many European countries.

Several factors are driving growth in the Europe cold sore treatment market. Firstly, the increasing awareness about cold sores, their causes, and treatments has led to early diagnosis and better management. Public health campaigns and information from healthcare professionals have improved consumer understanding of the importance of treatment adherence and virus transmission prevention. Secondly, the development of advanced formulations, including liposomal delivery and herbal-based treatments, is expanding product offerings and attracting consumers seeking alternatives to traditional antivirals.

The rising prevalence of HSV-1 among the European population is a significant growth driver. HSV-1 affects more than 60% of adults in many European countries, according to epidemiological studies. While most infections are asymptomatic, cold sore outbreaks cause physical discomfort, social embarrassment, and reduced quality of life, prompting individuals to seek effective treatments. Recurring infections are common, leading to repeat purchases and driving the demand for both preventive and therapeutic products.

Growing adoption of telemedicine and e-prescription services across Europe has improved patient access to antiviral medications and consultation services. Healthcare digitization, especially after the COVID-19 pandemic, has reshaped the way patients interact with providers and manage recurring conditions like cold sores. Many pharmaceutical companies are leveraging digital channels to promote awareness, offer virtual support, and facilitate product purchases.

Geographically, Western Europe dominates the cold sore treatment market due to higher healthcare spending, availability of advanced products, and favorable reimbursement structures in countries like Germany, France, and the UK. Germany holds the largest share due to strong pharmaceutical R&D, widespread availability of both OTC and prescription cold sore treatments, and increasing public awareness. France and the UK are also prominent markets, supported by a strong retail pharmacy network and proactive consumer behavior toward skin and oral health.

Eastern Europe, while currently a smaller market, is expected to grow steadily over the coming years. Increasing healthcare access, economic improvements, and growing awareness in countries such as Poland, Hungary, and Romania are driving product demand. Multinational pharmaceutical companies are expanding their footprint in the region through partnerships, marketing campaigns, and localized product launches.

The competitive landscape of the Europe cold sore treatment market is characterized by the presence of both global and regional players. Key market participants include GlaxoSmithKline plc, Mylan N.V., Novartis AG, Sun Pharmaceutical Industries Ltd., Teva Pharmaceutical Industries Ltd., and Valeant Pharmaceuticals. These companies are actively engaged in product innovation, strategic collaborations, and expanding their product availability across various European markets.

In addition to traditional antivirals, there is growing interest in plant-based and natural formulations. Products containing propolis, lysine, and essential oils are increasingly available as over-the-counter options and are favored by consumers who prefer chemical-free alternatives. While these products generally have lower clinical efficacy than prescription drugs, they cater to a niche segment of the population and contribute to market diversity.

Challenges in the Europe cold sore treatment market include limited awareness in some parts of Eastern Europe, the stigma associated with HSV infections, and competition from unregulated herbal products with questionable efficacy. Additionally, the development of resistance to existing antivirals and the lack of a definitive cure for HSV-1 highlight the need for continued innovation and research.

Source: https://www.databridgemarketresearch.com/reports/europe-cold-sore-treatment-market

In conclusion, the Europe cold sore treatment market is expected to grow steadily through 2033, driven by increased awareness, better healthcare access, expanding product categories, and technological innovation. As consumer expectations evolve and the demand for effective, fast-acting, and discreet treatment solutions continues to rise, manufacturers that focus on R&D, product accessibility, and patient-centric marketing will be best positioned for long-term success.

:

https://in.pinterest.com/

:

https://in.pinterest.com/